Income Tax Refund FY 2025-26 – Why Every Taxpayer Must Understand Refund Laws Carefully

For salaried employees, freelancers, professionals, startups, MSMEs, traders, NRIs, consultants, and growing businesses across India, income tax refund has become one of the most searched tax topics on Google.

Thousands of taxpayers file their Income Tax Return expecting a refund. However, many refunds are:

- delayed,

- adjusted against old demand,

- withheld during scrutiny,

- blocked due to defective returns,

- reduced after processing under Section 270 of Income Tax Act 2025,

- or entirely denied because of mismatches.

In FY 2025-26, refund scrutiny has become significantly stricter due to:

- AIS monitoring,

- TDS/TCS reconciliation systems,

- PAN-Aadhaar analytics,

- GST linkage,

- banking data verification,

- and automated risk management systems.

Many taxpayers believe refund is automatic. In reality, refund is a legal outcome of correct compliance.

This detailed guide explains:

- What is income tax refund?

- Relevant sections under Income Tax Act 1961 & Income Tax Act 2025

- Time limits for refund processing

- Notices affecting refund

- Reasons for refund delay

- Rules for withholding refund

- Interest on refund

- Refund adjustment against demand

- Real professional case studies resolved by Team Rokadh

- 30+ common refund mistakes

- 50+ most searched FAQs

Throughout this guide, Team Rokadh explains how taxpayers can legally protect refunds and avoid future tax litigation.

What is Income Tax Refund?

Income Tax Refund means excess tax paid by a taxpayer to the Income Tax Department beyond actual tax liability.

Refund may arise because of:

- Excess TDS deduction by employer

- Higher advance tax payment

- Wrong tax estimation

- TCS credits

- Foreign tax credit mismatch

- Self-assessment tax paid in excess

- Relief claims

- Capital loss adjustments

- Deduction claims

Under both the Income Tax Act 1961 and the proposed Income Tax Act 2025 framework, refund is processed after return assessment and verification.

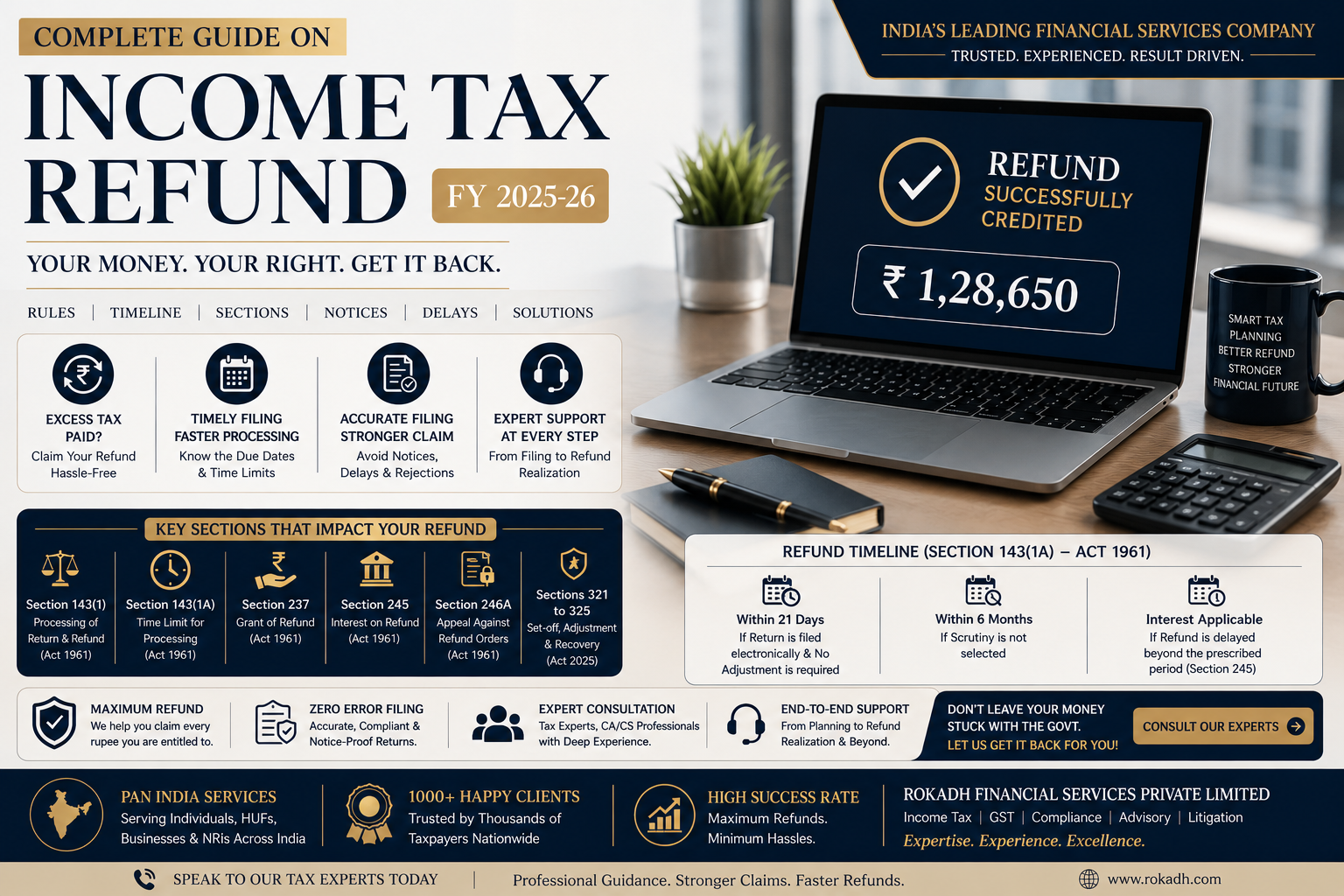

Relevant Sections Governing Income Tax Refund

Under Income Tax Act 1961

- Section 237 – Refunds

- Section 238 – Person entitled to claim refund

- Section 239 – Claim for refund

- Section 143(1) – Processing of return

- Section 143(2) – Scrutiny notice

- Section 245 – Adjustment of refund against demand

- Section 244A – Interest on refund

- Section 139 – Filing of return

- Section 139(5) – Revised return

- Section 139(8A) – Updated return

- Section 148 – Income escaping assessment

Under Income Tax Act 2025

Section 270 – Processing of Return & Refund Determination

Section 270 clearly explains:

- adjustments allowed while processing return,

- determination of refund,

- issuance of intimation,

- and processing timelines.

Under Section 270(1)(c), refund is determined after considering:

- TDS,

- TCS,

- advance tax,

- self-assessment tax,

- rebate,

- relief,

- and other tax payments.

Section 270(1)(e) specifically states that refund due shall be granted to the assessee.

Section 438 – Set Off & Withholding of Refund

Section 438 empowers department to:

- adjust refund against old demand,

- withhold refund during pending assessment/reassessment,

- or delay release after recording reasons.

However:

- written intimation is mandatory,

- approval from higher authority is necessary,

- and arbitrary withholding is not permissible.

Section 263 – Return Filing Compliance

Refund eligibility depends heavily upon valid return filing under Section 263.

Late filing, non-verification, defective returns, or invalid returns can directly impact refund processing.

How Income Tax Refund is Processed

The refund cycle generally follows these stages:

- ITR filing

- Verification of ITR

- Processing under Section 270 / Section 143(1)

- Adjustment checks

- AIS/TIS reconciliation

- Refund approval

- Bank validation

- Refund credit

If mismatch exists, department may issue:

- defective return notice,

- adjustment communication,

- scrutiny notice,

- reassessment notice,

- or refund withholding intimation.

Time Limit for Processing Refund

Under Income Tax Act 2025 – Section 270(4)

No intimation under Section 270(1) can be sent after:

9 months from end of financial year in which return is filed.

Example:

If return is filed on: 15 July 2025

Financial year ends: 31 March 2026

Refund processing timeline generally extends up to: 31 December 2026.

Interest on Income Tax Refund

Section 244A of Income Tax Act 1961

Taxpayer becomes eligible for interest when refund is delayed beyond prescribed period.

Interest generally applies when:

- excess advance tax paid,

- excess TDS deducted,

- refund delayed by department.

However:

Interest may be denied where delay is attributable to taxpayer.

Can Refund be Adjusted Against Old Demand?

Yes.

Section 245 (Income Tax Act 1961)

Section 438 (Income Tax Act 2025)

Department may adjust refund against:

- old outstanding demand,

- reassessment demand,

- penalty demand,

- interest liability.

But prior intimation is compulsory.

Many taxpayers ignore adjustment notices assuming refund will automatically come. That mistake often converts refund into litigation.

Real Case Story 1 – Salary Employee Refund Blocked Due to Old Demand

A senior software engineer from Pune approached Team Rokadh after waiting nearly 11 months for refund of ₹2,18,740.

His refund status continuously reflected:

“Refund determined and kept on hold due to outstanding demand.”

He had no knowledge about any old demand.

After detailed reconciliation, Team Rokadh identified:

- old AY mismatch from previous employer,

- incorrect TDS credit reflection,

- duplicated Form 16 entry.

Department had raised demand of ₹3,41,900.

The taxpayer was under severe stress because:

- home loan EMI was pending,

- refund was financially important,

- and notices were continuously being generated.

Team Rokadh:

- prepared rectification,

- reconciled Form 26AS,

- drafted legal response,

- submitted supporting payroll records,

- and handled portal follow-up.

Final Outcome:

- Wrong demand deleted

- Refund released

- Interest under Section 244A granted

- Final refund credited: ₹2,34,180

Internal Compliance Support

If your refund is blocked due to old demand, Team Rokadh professionally handles:

- refund rectification,

- demand reconciliation,

- notice drafting,

- refund release representation,

- and faceless proceedings.

Notices That Commonly Affect Refund

1. Section 143(1) / Section 270 Adjustment Notice

Issued when:

- TDS mismatch exists,

- deduction appears excessive,

- losses incorrectly claimed,

- audit mismatch identified.

Possible Consequences:

- refund reduction,

- demand creation,

- interest liability.

2. Section 139(9) Defective Return Notice

Issued when:

- return incomplete,

- audit report missing,

- schedules incomplete,

- mismatch in financial reporting.

If ignored:

Return may become invalid. Refund may fail entirely.

3. Section 143(2) Scrutiny Notice

Issued where department seeks detailed verification.

Consequences may include:

- refund withholding,

- reassessment,

- penalty proceedings.

4. Section 148 / Section 280 Reassessment Notice

Issued where income escaped assessment.

Refunds may be frozen during reassessment proceedings.

5. Section 245 / Section 438 Refund Adjustment Notice

Issued before refund set-off.

Taxpayer must respond immediately.

Real Case Story 2 – Freelancer Received Refund Reduction Notice

A digital marketing consultant from Ahmedabad filed ITR claiming refund of ₹4,92,600.

Within weeks, an adjustment notice was issued.

Department proposed disallowance because:

- TDS entries mismatched,

- two clients deducted TDS under wrong PAN,

- and one invoice was duplicated.

The consultant panicked after seeing proposed tax demand crossing ₹6 lakh.

Team Rokadh conducted:

- complete ledger reconciliation,

- client coordination,

- revised TDS correction,

- AIS correction support,

- and legal response filing.

Result:

- proposed demand dropped substantially,

- refund protected,

- final refund received: ₹4,41,380.

Internal Linking & CTA

Facing refund reduction notice? Team Rokadh provides PAN India support for:

- Section 270 replies,

- AIS mismatch handling,

- TDS reconciliation,

- refund litigation,

- and faceless assessments.

Refund Withholding During Scrutiny

Under Section 438(3), refund may be withheld where:

- assessment/reassessment pending,

- officer records reasons in writing,

- higher authority approval obtained.

However, withholding cannot be arbitrary.

Taxpayers have legal rights.

Real Case Story 3 – Startup Founder Refund Withheld During Assessment

A SaaS startup founder from Bengaluru claimed refund of ₹18,46,000 after startup losses and TDS credits.

Department initiated scrutiny over:

- ESOP accounting,

- foreign remittances,

- expense classifications,

- startup valuation mismatch.

Refund was withheld.

Investor pressure increased. Cash flow became critical.

Team Rokadh:

- prepared detailed submissions,

- reconciled FEMA-linked transactions,

- structured expense justifications,

- coordinated with startup accountants,

- and represented during faceless assessment.

Final Result:

- no major additions sustained,

- refund partially released during proceedings,

- final refund with interest exceeded ₹19 lakh.

Strategic Compliance Advisory

Startups receiving notices regarding refunds, foreign funding, ESOPs, or expense scrutiny should immediately seek professional representation.

Team Rokadh handles:

Common Reasons Why Refund Gets Delayed

1. PAN-Aadhaar not linked

2. Return not verified

3. Wrong bank account

4. AIS mismatch

5. TDS mismatch

6. Defective return

7. High-value transaction mismatch

8. Pending demand

9. Scrutiny selection

10. Revised return conflict

11. Updated return complications

12. Foreign asset disclosure mismatch

Revised Return & Updated Return Impact on Refund

Revised Return – Section 139(5) / Section 263(5)

Allowed when:

- omission discovered,

- wrong statement identified.

Can help correct:

- refund amount,

- deduction claims,

- TDS mismatch.

Updated Return – Section 139(8A) / Section 263(6)

Updated return generally cannot:

- increase refund,

- reduce tax liability.

Many taxpayers wrongly assume updated return can be used to increase refund.

Law restricts such usage.

Real Case Story 4 – Wrong Updated Return Caused Refund Crisis

A trader from Surat attempted filing updated return himself after discovering missing TDS entries.

He expected higher refund.

Instead:

- updated return became legally defective,

- refund processing stopped,

- notice risk increased.

Team Rokadh reviewed the matter and identified:

- updated return was legally impermissible for refund enhancement,

- revised return timeline had already expired.

Strategic representation and rectification were undertaken.

Result:

- penalty exposure minimized,

- refund issue resolved through alternative compliance route,

- future litigation avoided.

Compliance Support

Before filing revised or updated return, professional review is critical.

Team Rokadh assists in:

Consequences of Wrong Refund Claim

Wrong or excessive refund claims may trigger:

- adjustment notices,

- scrutiny,

- reassessment,

- penalties,

- prosecution in extreme cases.

Especially risky areas include:

- fake deductions,

- manipulated TDS,

- artificial losses,

- fake HRA,

- bogus donations.

30+ Common Refund Mistakes

1. Claiming TDS Without Actual Reflection in Form 26AS

One salaried employee from Pune claimed TDS of ₹2,84,000 based on salary slips while the employer had deposited only partial tax. The refund was automatically reduced and the taxpayer received mismatch communication.

The taxpayer initially attempted self-response through the portal which worsened the reconciliation issue.

Team Rokadh:

- reconciled Form 26AS,

- identified defaulting deductor,

- coordinated revised TDS return,

- drafted professional representation,

- and secured refund release with applicable interest.

CTA: Taxpayers should never assume salary slip equals valid TDS credit. Before filing refund claims, get professional TDS verification through Rokadh Financial Services Private Limited.

2. Incorrect Bank Account Validation Causing Refund Failure

A startup founder from Bengaluru waited almost 14 months for refund release because the bank account linked with PAN was inactive.

Repeated refund reissues failed.

Team Rokadh:

- validated updated bank accounts,

- corrected pre-validation issues,

- filed refund reissue requests,

- tracked CPC communications,

- and resolved complete refund blockage.

CTA: Even small technical mistakes can block lakhs of refund. Team Rokadh provides PAN India refund monitoring and correction services.

3. Ignoring AIS-TIS Mismatch Notices

A consultant ignored AIS mismatch related to foreign remittance and crypto transactions believing it was “system generated only.”

Later reassessment proceedings were initiated.

Team Rokadh:

- analysed AIS/TIS data,

- reconciled transaction trail,

- prepared legal submissions,

- corrected disclosure mismatch,

- and minimised proposed addition substantially.

CTA: AIS/TIS mismatches are one of the biggest triggers for refund hold and scrutiny in FY 2025-26. Professional response drafting is critical.

4. Filing Revised Return Incorrectly

A taxpayer revised return multiple times without understanding tax impact.

This triggered inconsistency alerts under processing provisions.

Team Rokadh:

- reviewed all prior filings,

- mapped revised computations,

- corrected deduction claims,

- filed structured reconciliation,

- and prevented escalation into scrutiny.

CTA: Improper revised returns can create bigger litigation than original mistakes. Team Rokadh ensures strategic revision planning.

5. Wrong Foreign Asset Disclosure

An NRI-returning resident failed to disclose foreign brokerage holdings.

The matter escalated due to information-sharing mechanisms.

Team Rokadh:

- assessed residential status,

- prepared foreign asset disclosures,

- structured legal submissions,

- and prevented severe penal consequences.

CTA: Foreign asset reporting errors are now aggressively monitored. High-net-worth taxpayers should seek specialised compliance support from Team Rokadh.

6. Filing return without verification

A salaried taxpayer assumed OTP verification was optional. Refund remained stuck for months until Team Rokadh completed compliance restoration.

7. Wrong bank account details

Incorrect IFSC caused refund failure despite processing completion.

8. Ignoring defective return notice

A consultant lost refund opportunity because Section 139(9) notice remained unanswered.

9. Wrong HRA claim

Fake rent declaration created refund reversal risk.

10. Unsupported 80D deduction

Medical insurance claim lacked documentation.

11. Claiming fake donations

Unverified donation receipts triggered scrutiny.

12. Ignoring TDS mismatch

Form 26AS mismatch reduced refund significantly.

13. Wrong residential status declaration

NRI income disclosure errors created reassessment exposure.

14. Failure to disclose foreign shares

Foreign brokerage holdings not disclosed in Schedule FA.

15. Improper depreciation claim

Business owner claimed excess depreciation causing adjustment notice.

16. Non-maintenance of books

Freelancer lacked expense records during scrutiny.

17. Personal expenses claimed as business expenses

Luxury travel claimed as business expenditure.

18. Fake agricultural income claim

Artificial agricultural income used to suppress tax.

19. Improper partner remuneration claim

Partnership deed mismatch triggered disallowance.

20. Wrong inventory valuation

Closing stock manipulation increased scrutiny risk.

21. Mismatch between audit report and ITR

Tax audit figures differed from filed return.

22. Non-disclosure of mutual fund redemption

Capital gains omitted accidentally.

23. Ignoring reassessment timelines

Late response increased legal exposure.

24. Wrong bank reporting for refund credit

Dormant account linked in return.

25. Unreported rent income

Rental receipts reflected in AIS but not ITR.

26. Incorrect set-off of losses

Expired losses adjusted wrongly.

27. Duplicate deduction claims

Same investment claimed twice.

28. Incorrect self-assessment tax challan

Wrong AY selected while payment.

29. Failure to reconcile AIS

Large transactions remained unexplained.

30. Ignoring compliance emails

Taxpayer believed emails were spam.

31. Wrong presumptive taxation usage

Ineligible business opted presumptive scheme.

32. Claiming exempt income without proof

Tax-free claims unsupported.

33. Wrong capital gain calculation

Brokerage statements misunderstood.

34. Delayed revised return filing

Correction timeline expired.

35. Filing return using estimated figures

Final Form 16 figures later changed.

36. Wrong carry forward of losses

Loss return filed beyond due date.

37. Non-reporting crypto transactions

Virtual asset transactions surfaced through analytics.

38. Cash deposits mismatch

Banking data triggered automated notices.

39. Incorrect GST turnover reporting

GST turnover mismatched with ITR turnover.

40. Ignoring refund adjustment intimation

Refund got adjusted unnecessarily.

All these situations were:

- educated,

- awared,

- strategically guided,

- legally represented,

- reconciled,

- and resolved by Team Rokadh.

50+ Most Searched FAQs on Income Tax Refund

1. Can income tax refund be stopped without notice?

In many situations, yes. Refunds may be withheld where assessment or reassessment proceedings are pending and the department believes recovery protection is necessary.

However, such withholding generally requires reasons recorded in writing and approvals under applicable law.

Team Rokadh regularly assists taxpayers in:

- obtaining refund status clarity,

- challenging unlawful withholding,

- drafting representations,

- reconciling prior demands,

- and accelerating refund processing.

CTA: If your refund is “under processing” for unusually long periods, immediate professional intervention may help avoid future litigation.

2. Can old tax demand reduce current refund?

Yes. Under refund adjustment provisions, old outstanding demands may be adjusted against current refund.

Many taxpayers discover historic demands only after refund adjustment intimation.

Team Rokadh helps in:

- demand verification,

- rectification applications,

- old challan reconciliation,

- stay applications,

- and removal of incorrect legacy demands.

CTA: Do not ignore old tax demands shown on portal. Even invalid historical demands can silently consume your refund.

3. Can freelancers and digital creators receive refund scrutiny?

Absolutely.

The department now tracks:

- UPI credits,

- foreign remittances,

- ad revenues,

- affiliate income,

- crypto transactions,

- and platform-based receipts.

Team Rokadh has assisted numerous:

- freelancers,

- YouTubers,

- consultants,

- influencers,

- startup founders,

- and professionals

in reconciling digital income and protecting refund claims.

CTA: Digital economy taxpayers face significantly increased compliance monitoring in FY 2025-26.

4. What happens if refund claim is excessive?

Excessive refund claims may lead to:

- processing adjustments,

- scrutiny notices,

- reassessment,

- penalty exposure,

- refund withholding,

- and prosecution risk in extreme situations.

Team Rokadh helps taxpayers proactively:

- verify deductions,

- reconcile TDS,

- correct disclosures,

- and minimise future litigation exposure.

CTA: Aggressive refund filing without compliance verification can create long-term legal consequences.

5. Why are salaried taxpayers receiving notices despite TDS deduction?

Modern compliance systems compare:

- salary income,

- AIS/TIS,

- high-value transactions,

- mutual fund redemptions,

- foreign remittances,

- property purchases,

- and interest income.

Even fully salaried taxpayers now receive notices due to data mismatches.

Team Rokadh assists salaried employees in:

CTA: Salary income alone no longer guarantees notice-free filing. Accurate disclosure and strategic compliance have become essential.

6. How long does income tax refund take?

Generally processed after return verification and Section 270/143(1) processing.

7. Can refund be delayed beyond one year?

Yes, especially during scrutiny or mismatch cases.

8. What is Section 270 adjustment?

Adjustment during return processing for apparent errors or mismatches.

9. Can refund be stopped during scrutiny?

Yes, under Section 438.

10. Can old demand block refund?

Yes.

11. Is prior notice mandatory before refund adjustment?

Yes.

12. Can revised return increase refund?

Yes, within permitted timeline.

13. Can updated return increase refund?

Generally no.

14. Is refund taxable?

Refund itself no, interest may be taxable.

15. What is refund interest?

Interest under Section 244A.

16. Can refund include TDS mismatch correction?

Yes.

17. Can freelancers receive scrutiny notices?

Absolutely.

18. Can AIS mismatch reduce refund?

Yes.

19. What if refund credited to wrong account?

Immediate rectification required.

20. Can refund fail because of PAN-Aadhaar issue?

Yes.

21. Can refund come after reassessment?

Yes, subject to proceedings.

22. Can refund be manually released?

Certain cases require representation.

23. What if employer deducted excess TDS?

Refund may be claimed.

24. What if TDS missing in Form 26AS?

Correction from deductor may be required.

25. Can startup founders receive refund scrutiny?

Yes.

26. Is notice reply drafting important?

Very important legally.

27. Can refund be rejected entirely?

Yes, in defective or invalid return cases.

28. What is defective return notice?

Notice seeking correction of incomplete return.

29. Can refund trigger scrutiny?

High refund claims may attract verification.

30. Can crypto transactions affect refund?

Yes.

31. Is foreign asset disclosure mandatory?

For eligible residents, yes.

32. Can capital loss increase refund?

Legitimate loss set-off may reduce tax.

33. What if refund status says processed but not received?

Bank validation or adjustment issue may exist.

34. Can GST mismatch impact refund?

Yes.

35. Is faceless assessment applicable?

Yes in many cases.

36. Can Team Rokadh handle faceless notices?

Yes.

37. What if response deadline missed?

Immediate legal strategy required.

38. Can refund be reissued?

Yes in eligible cases.

39. Can refund adjustment be challenged?

Yes.

40. Can wrong deductions create penalty?

Potentially yes.

41. What if return not verified?

Return may become invalid.

42. Can refund include self-assessment tax?

Yes.

43. Is notice through email valid?

Yes.

44. Can refund get withheld without approval?

Law requires approval.

45. What if ITR and audit report mismatch?

Adjustment or scrutiny possible.

46. Can refund processing happen automatically?

Many cases are system-driven.

47. Can legal drafting reduce demand?

Strong documentation matters significantly.

48. Can old notices affect future refunds?

Yes.

49. Is interest mandatory on delayed refund?

Subject to conditions.

50. Can reassessment reopen closed refund years?

Yes under law.

51. What if deduction proof unavailable?

Claim may fail.

52. Can refund issue affect loan approval?

Pending demands may impact financial profile.

53. How to avoid refund notices?

Proper reconciliation and compliance.

54. Can Team Rokadh represent in appeals?

Yes.

55. Can refund disputes be resolved at NIL demand?

In many cases, yes through proper representation.

56. Is professional assistance necessary for high-value refunds?

Strongly advisable.

57. Can business owners face refund scrutiny more frequently?

Yes due to turnover analytics.

58. Can multiple revised returns create complications?

Yes.

59. What if refund remains pending for very long?

Escalation and representation may be required.

60. How can taxpayers stay compliant?

Timely filing, reconciliation, and professional review.

All these refund-related questions have been:

- educated,

- awared,

- strategically guided,

- legally represented,

- and resolved by Team Rokadh.

Final Conclusion

Income tax refund is not merely a banking transaction. It is a compliance-driven legal process governed by:

- Income Tax Act 1961 upto FY 2025-26,

- Income Tax Act 2025 form FY 2026-27 onward,

- processing rules,

- reassessment provisions,

- refund adjustment powers,

- and scrutiny procedures.

A single mismatch can:

- delay refund,

- trigger notices,

- create demand,

- initiate reassessment,

- or lead to prolonged litigation.

Taxpayers across India must therefore:

- reconcile AIS,

- verify TDS,

- disclose income properly,

- respond to notices timely,

- and maintain documentation carefully.

Professional Support by Rokadh Financial Services Private Limited

Rokadh Financial Services Private Limited supports taxpayers PAN India in:

- Income Tax Return Filing

- Refund Litigation

- Section 270 Replies

- Scrutiny Representation

- Reassessment Defense

- AIS/TIS Reconciliation

- Refund Release Matters

- Faceless Assessments

- Startup Tax Advisory

- MSME Tax Compliance

- Appeal Drafting

- High-Value Refund Cases

Whether you are:

- salaried employee,

- startup founder,

- trader,

- freelancer,

- MSME owner,

- NRI,

- or professional,

Team Rokadh helps taxpayers stay compliant, protected, and financially secure.

Internal Linking Suggestions

- Complete Guide to Income Tax Notices in India

- GST Notices & Departmental Actions

- GSTR-1 Complete Compliance Guide

- GSTR-3B Complete Compliance Guide

- Startup Taxation & Notices

- AIS/TIS Reconciliation Services

- Faceless Assessment Representation

- Income Tax Appeal Drafting Services

- MSME Compliance Support