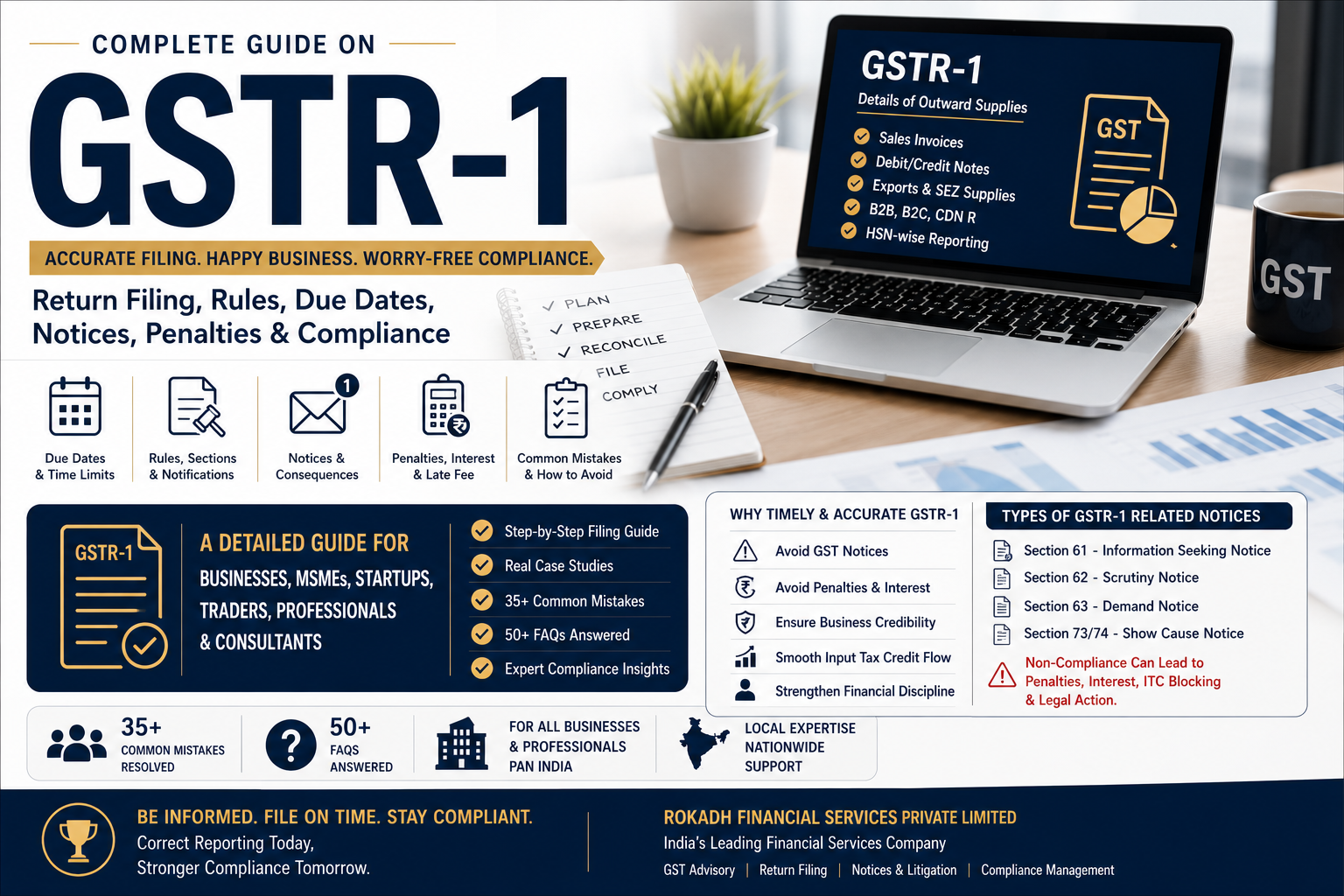

What is GSTR-1?

GSTR-1 is a monthly or quarterly return under the Goods and Services Tax (GST) law in which a registered taxpayer reports details of outward supplies (sales). It includes:

- B2B sales

- B2C sales

- Export invoices

- Credit notes

- Debit notes

- Advances received

- HSN-wise summary

- Nil-rated and exempt supplies

The return is filed under the provisions of:

- Section 37 of the CGST Act, 2017

- Rule 59 of the CGST Rules, 2017

GSTR-1 forms the foundation of the GST compliance system because:

- Buyer’s Input Tax Credit (ITC) depends upon supplier’s GSTR-1.

- Mismatch may trigger notices.

- Incorrect filing may lead to penalties, scrutiny, demand notices, cancellation proceedings, and GST investigations.

For Expert Support, book appointment as GST Consultation Services

Why GSTR-1 Filing is Extremely Important

Many businesses wrongly assume that GST liability is determined only through GSTR-3B. However, GST authorities now use advanced data analytics to compare:

- GSTR-1

- GSTR-3B

- E-way bills

- E-invoices

- Income Tax returns

- TDS/TCS data

- Banking transactions

Even a small mismatch may trigger automated notices.

A single incorrect invoice can:

- Block buyer’s ITC

- Trigger vendor disputes

- Create GST demand

- Cause interest and penalty exposure

- Lead to scrutiny under Section 61

- Trigger inspection under Section 67

Legal Provisions Governing GSTR-1

Section 37 of CGST Act

Every registered person (except composition dealer, ISD, TDS/TCS deductors and certain others) must furnish details of outward supplies electronically.

Rule 59 of CGST Rules

Specifies:

- Manner of filing

- Invoice reporting structure

- Amendment mechanism

- IFF filing for QRMP taxpayers

Who Must File GSTR-1?

The following taxpayers are generally required to file GSTR-1:

- Proprietorship businesses

- Partnership firms

- LLPs

- Private limited companies

- Freelancers registered under GST

- E-commerce sellers

- Exporters

- Service providers

- Consultants

- Manufacturers

- Traders

Even if there are no sales, NIL GSTR-1 may still be required.

Monthly vs Quarterly GSTR-1 Filing

Monthly Filing

Businesses with turnover exceeding prescribed QRMP limit must file monthly.

Due Date:

11th of next month.

Example:

April sales → GSTR-1 due by 11th May.

Quarterly Filing under QRMP Scheme

Businesses eligible under QRMP may file quarterly.

Due Date:

13th of month following quarter.

Example:

April–June quarter → due by 13th July.

Turnover Threshold for QRMP Scheme

Businesses with aggregate turnover up to ₹5 crore may opt for QRMP.

However:

- Tax payment may still be monthly.

- Invoice Furnishing Facility (IFF) may be used for B2B invoices.

Major Components of GSTR-1

1. B2B Invoices

Invoices issued to registered persons.

Includes:

- GSTIN of recipient

- Invoice number

- Taxable value

- GST amount

- Place of supply

Common Issue:

Wrong GSTIN entry causing ITC denial to customer.

Real Case Story

A machinery trader from Pune uploaded invoices worth ₹48,75,000 with one digit incorrect in recipient GSTIN.

Customer blocked payment of ₹8.7 lakh due to ITC mismatch.

GST department later issued mismatch communication.

Team Rokadh:

- reconciled invoice data,

- amended GSTR-1,

- coordinated with buyer,

- rectified reporting cycle,

- restored ITC flow.

Potential litigation exposure reduced significantly.

Need Professional Reconciliation?

Explore GST reconciliation and notice handling support from Rokadh Financial Services Private Limited for accurate monthly compliance.

2. B2C Large Invoices

Invoices issued to unregistered persons exceeding threshold limits for interstate supply.

Improper reporting may trigger analytics-based notices.

3. B2C Small Supplies

Consolidated reporting for retail transactions.

Commonly used by:

- Retail stores

- Restaurants

- Local traders

- Small manufacturers

4. Credit Notes & Debit Notes

Reported separately.

Used when:

- Sales return occurs

- Rate correction required

- Invoice value changes

- Discount issued post sale

Improper credit note reporting is among the most common GST litigation triggers.

5. Export Supplies

Includes:

- LUT exports

- IGST paid exports

- SEZ supplies

Export mismatch frequently leads to refund blockage.

Real Case Story

An exporter from Surat filed export invoices in GSTR-1 but shipping bill mismatch caused refund blockage of ₹31.4 lakh.

The issue continued for 8 months.

Team Rokadh:

- reconciled ICEGATE data,

- corrected invoice references,

- coordinated with GST officer,

- rectified shipping mismatches,

- reopened refund processing.

Refund with interest was later processed.

Facing Export GST Issues?

Rokadh Financial Services Private Limited assists exporters across India with LUT filing, refund processing, reconciliation and litigation management.

How to File GSTR-1

Step-by-Step Process

Step 1: Login to GST Portal

Access:

- GST portal

- Return dashboard

- Select period

Step 2: Choose GSTR-1

Select relevant tax period.

Step 3: Upload Invoice Data

Report:

- B2B invoices

- B2C sales

- Exports

- Credit notes

- Debit notes

Step 4: Validate Data

Cross-check:

- GSTIN

- Invoice number

- Tax amount

- POS

- HSN code

Step 5: Submit Return

Preview return before filing.

Step 6: File Using DSC/EVC

Return becomes final after filing.

Invoice Furnishing Facility (IFF)

QRMP taxpayers may upload B2B invoices monthly through IFF.

Due Date:

13th of succeeding month.

Failure may impact buyer ITC.

Amendment in GSTR-1

Mistakes can be corrected through amendment tables.

However, correction timelines are restricted.

Time Limit for GSTR-1 Amendments

Corrections generally allowed up to:

- 30th November following financial year

- OR

- date of annual return filing,

- whichever is earlier.

Delayed corrections may permanently block adjustments.

Common Notices Related to GSTR-1

1. Section 61 – Scrutiny Notice

Issued when department identifies mismatch.

Common Triggers:

- GSTR-1 vs GSTR-3B mismatch

- ITC irregularity

- E-way bill inconsistency

- Abnormal turnover fluctuations

Time Limit

No fixed limitation specifically prescribed for scrutiny initiation, but scrutiny generally starts post return review.

Consequences

- Demand proceedings

- Interest

- Penalty

- Further investigation

Real Story

A trader declared outward supplies of ₹2.8 crore in GSTR-1 but paid tax on ₹1.9 crore in GSTR-3B.

Automated scrutiny notice issued.

Team Rokadh identified:

- duplicate invoice uploads,

- omitted amendments,

- reporting confusion between branches.

After detailed reply and reconciliation:

Final additional liability reduced substantially.

Need Notice Reply Drafting?

Rokadh Financial Services Private Limited handles GST scrutiny notices, reconciliations and departmental representation across India.

2. Section 73 Notice

Issued for non-fraud cases involving short payment.

Time Limit

Generally within prescribed statutory limitation from due date of annual return.

Consequences

- Tax demand

- Interest

- Penalty

3. Section 74 Notice

Issued where department alleges fraud, suppression or wilful misstatement.

Consequences

Very serious:

- 100% penalty exposure

- Recovery proceedings

- Bank attachment

- Investigation risk

Real Story

A wholesaler received allegation of fake billing involving ₹1.84 crore.

Department proposed tax + penalty exceeding ₹92 lakh.

Team Rokadh:

- reconstructed purchase trail,

- validated transport records,

- produced payment proofs,

- reconciled vendor GST filings.

Case exposure reduced dramatically after detailed defense.

Facing High-Risk GST Notice?

Professional drafting and evidence management can significantly impact litigation outcomes. Rokadh assists businesses PAN India in GST disputes and investigations.

4. DRC-01 Notice

Show cause notice for tax demand.

Requires detailed legal reply.

Ignoring DRC-01 often escalates recovery proceedings.

5. ASMT-10 Notice

Issued for discrepancies noticed during scrutiny.

Must be replied within specified timeline.

Late Filing Consequences

Late Fee

Applicable per day of delay subject to prescribed limits.

Interest Liability

Interest may apply on delayed tax payment.

Serious Risks of Non-Filing

Continuous non-filing may lead to:

- GST cancellation

- Blocking of e-way bills

- Buyer ITC disputes

- Recovery proceedings

- Bank attachment

- Department audit

- Business credibility damage

Real Case Study – Non-Filing Crisis

A construction contractor ignored GST filings for 11 months due to cash flow issues.

Consequences:

- GST registration suspension

- Vendor payment blockage

- ITC denial to customers

- Multiple notices

Team Rokadh:

- reconstructed books,

- prepared pending returns,

- negotiated payment planning,

- restored compliance continuity,

- assisted revocation process.

Business operations resumed gradually.

Delayed GST Returns?

Rokadh Financial Services Private Limited supports taxpayers in return reconstruction, notice handling and revocation matters across India.

30+ Common GSTR-1 Mistakes

1. Wrong GSTIN Upload

Buyer unable to claim ITC.

Team Rokadh reconciled and amended invoices professionally.

2. Reporting B2B as B2C

Created major ITC disputes.

Resolved through amendment mechanism.

3. Non-Reporting of Credit Notes

Tax liability became inflated.

Corrected through revised reporting.

4. Wrong HSN Codes

Triggered departmental analytics mismatch.

Resolved through HSN correction strategy.

5. Duplicate Invoice Upload

Created excess turnover reflection.

Reconciled by Team Rokadh.

6. Missing Export Invoices

Refund blocked.

Resolved after ICEGATE reconciliation.

7. Incorrect Place of Supply

Wrong tax type paid.

Corrected through amendment filings.

8. Ignoring Section 61 Notice

Escalated to demand proceedings.

Handled through structured legal response.

9. Delay in Filing GSTR-1

Buyer relationships damaged due to ITC blockage.

Team Rokadh regularized filings.

10. Non-Reconciliation with GSTR-3B

Triggered automated notices.

Reconciled professionally.

11. Wrong Tax Rate Application

Underpayment exposure created.

Corrected with interest optimization.

12. Ignoring E-way Bill Mismatch

Led to investigation risk.

Resolved through transaction mapping.

13. Missing Debit Notes

Tax shortfall occurred.

Rectified through amendments.

14. Incorrect Amendments

Further mismatch created.

Resolved through expert correction strategy.

15. Filing Without Review

Massive reporting errors occurred.

Team Rokadh introduced maker-checker controls.

16. Unreported Advances

Tax exposure increased.

Resolved with proper adjustment entries.

17. Wrong Export Category

Refund complications arose.

Corrected with export advisory support.

18. Ignoring Buyer Complaints

Escalated into notice disputes.

Resolved through coordinated reconciliation.

19. Incorrect Nil Return Filing

Sales existed but NIL return filed mistakenly.

Team Rokadh corrected exposure.

20. Mismatch with Books

Department flagged turnover inconsistency.

Resolved through complete reconciliation.

21. Wrong Branch Reporting

Inter-branch confusion created duplicate tax exposure.

22. Failure to Maintain Invoice Sequence

Compliance deficiency identified during scrutiny.

23. Ignoring GST Portal Errors

Returns remained partially filed.

24. Wrong Amendment Period Selection

Corrections failed technically.

25. Excessive Manual Data Entry

Human error caused multiple notices.

26. Non-Matching E-Invoice Data

Triggered analytics alerts.

27. Missing LUT Reporting

Export complications increased.

28. Late IFF Upload

Buyer ITC blocked temporarily.

29. Non-Disclosure of SEZ Supplies

Refund delay created.

30. Incorrect Taxable Value

Demand notice issued later.

31. Wrong Classification of Exempt Supply

Created reporting inconsistencies.

32. Non-Maintenance of Working Papers

Defense became difficult during litigation.

33. Ignoring Automated GST Communications

Escalation risk increased significantly.

All these issues were professionally educated, guided, reconciled and resolved by Team Rokadh through structured GST compliance management.

50+ Frequently Asked Questions

1. What is GSTR-1?

GSTR-1 is return of outward supplies under GST.

2. Who must file GSTR-1?

Most registered taxpayers except specified exempt categories.

3. What is due date for monthly filing?

11th of next month.

4. What is QRMP due date?

13th after quarter end.

5. Can NIL GSTR-1 be filed?

Yes.

6. Can GSTR-1 be revised?

Direct revision not allowed, but amendments possible.

7. What happens if GSTR-1 not filed?

Late fee, notices, suspension risk and ITC blockage.

8. Can wrong GSTIN be corrected?

Yes through amendments within permitted timelines.

9. What if buyer ITC blocked?

Invoice reconciliation required.

10. Can export invoices be amended?

Yes within legal timelines.

11. What is IFF?

Invoice Furnishing Facility for QRMP taxpayers.

12. Is GSTR-1 mandatory without sales?

Usually NIL filing required.

13. Can notices come automatically?

Yes. GST system is analytics driven.

14. What is Section 61 notice?

Scrutiny notice for discrepancies.

15. What is DRC-01?

Demand show cause notice.

16. Can GST registration cancel for non-filing?

Yes.

17. What if books unavailable?

Reconstruction may be required.

18. Can old mismatches trigger notices?

Yes.

19. Is interest mandatory?

Generally applicable on delayed payment.

20. Can penalties be waived?

Depends upon facts and response quality.

21. What if tax already paid?

Evidence submission required.

22. Can notices be replied online?

Yes in most cases.

23. Is personal hearing compulsory?

Depends on proceedings.

24. Can GSTR-1 mismatch trigger audit?

Yes.

25. What if invoice uploaded twice?

Amendment required.

26. Can buyer sue for ITC loss?

Commercial disputes may arise.

27. Is GST data linked with Income Tax?

Yes increasingly through analytics.

28. Can freelancers receive notices?

Absolutely.

29. Can startups receive scrutiny?

Yes.

30. Is legal drafting important?

Very important in litigation matters.

31. Can Team Rokadh handle notices?

Yes, PAN India support available.

32. Can GSTR-1 affect refund?

Directly.

33. What if HSN incorrect?

May trigger mismatch scrutiny.

34. Can e-way bill mismatch create notice?

Yes.

35. Can amendment be done after annual return?

Usually restricted.

36. Is DSC compulsory?

Depends on taxpayer category.

37. Can nil return be filed through SMS?

In eligible cases yes.

38. What if portal error occurs?

Document evidence immediately.

39. Can wrong POS create liability?

Yes.

40. What if GST paid under wrong head?

Adjustment/refund process may apply.

41. Can delayed filing affect rating?

Yes commercially.

42. Can GST department freeze bank account?

In serious proceedings yes.

43. Is reconciliation mandatory?

Practically essential.

44. What if customer denies invoice?

Evidence verification required.

45. Can old returns be reopened?

In certain proceedings yes.

46. Can export refund be rejected?

Yes due to mismatch.

47. What if business closed?

Returns and cancellation formalities still important.

48. Can notices be resolved at NIL demand?

In many genuine cases yes.

49. Can Team Rokadh represent before department?

Yes.

50. How to avoid future GST notices?

Proper reconciliation, timely filing and professional review.

51. Why choose professional GST management?

Because small compliance mistakes can become major litigation exposure later.

All these FAQs have been professionally educated, guided and resolved by Team Rokadh through structured GST compliance and litigation support services.

Final Professional Advisory

GSTR-1 is no longer a simple return filing formality.

It is now one of the most important compliance documents under GST law because every invoice is digitally tracked and reconciled by the department.

Businesses today face increasing risks from:

- automated notices,

- AI-based mismatch tracking,

- ITC disputes,

- departmental scrutiny,

- vendor reconciliation issues,

- refund blockage,

- litigation exposure.

Timely filing alone is not sufficient.

Accurate reconciliation, legal review, amendment tracking and notice management have become equally critical.

Need Professional GST Compliance Support?

Rokadh Financial Services Private Limited assists businesses, professionals, startups, exporters, manufacturers, traders and MSMEs across India with:

- GSTR-1 filing

- GST reconciliation

- GST notices

- Litigation management

- GST audit support

- Refund assistance

- Export GST advisory

- Department representation

- Compliance structuring

Stay compliant.

Protect your business credibility.

Reduce litigation exposure.

Strengthen GST compliance professionally.