Companies Compliance Facilitation Scheme, 2026 (CCFS-2026)

(General Circular No. 01/2026 dated 24 February 2026 issued by Ministry of Corporate Affairs)

India’s corporate ecosystem has crossed a historic milestone — more than 20 lakh active companies are now registered under the Companies Act, 2013. This surge reflects growing formalization, rising entrepreneurship, expanding MSMEs, and increasing compliance awareness.

However, with growth comes compliance pressure.

Under Sections 92 and 137 of the Companies Act, 2013, every company is required to file:

- Annual Return

- Financial Statements

And as per Section 403, delay in filing attracts ₹100 per day additional fee — without any upper limit.

For many MSMEs, startups, and private limited companies, this has resulted in massive financial burden over time.

Recognizing these hardships, the Ministry of Corporate Affairs (MCA) issued General Circular No. 01/2026 dated 24 February 2026, introducing:

Companies Compliance Facilitation Scheme, 2026 (CCFS-2026)

This scheme offers a one-time opportunity to regularize defaults at drastically reduced cost.

At Rokadh Financial Services Private Limited (www.rokadh.com), we believe this scheme can be transformational for thousands of companies — if acted upon within the prescribed timeline.

This blog provides a complete professional analysis of CCFS-2026 — eligibility, benefits, immunity provisions, exclusions, timelines, strategy, and practical guidance.

1. Why Was CCFS-2026 Introduced?

Over the years, MCA has received multiple representations from:

- MSMEs

- One Person Companies (OPCs)

- Producer Companies

- Private Limited Companies

- Inactive / defunct companies

Many were unable to complete annual filings on time due to:

- Lack of awareness

- Financial stress

- Change in management

- Dormant business operations

- Disputes among directors

- Technical filing complexities

The result?

Massive additional fees accumulated — often exceeding the company’s net worth.

To:

- Improve overall compliance levels

- Update corporate registry records

- Reduce burden on inactive entities

- Promote ease of doing business

The Central Government, exercising powers under Section 460 read with Section 403 of the Companies Act, 2013, launched CCFS-2026.

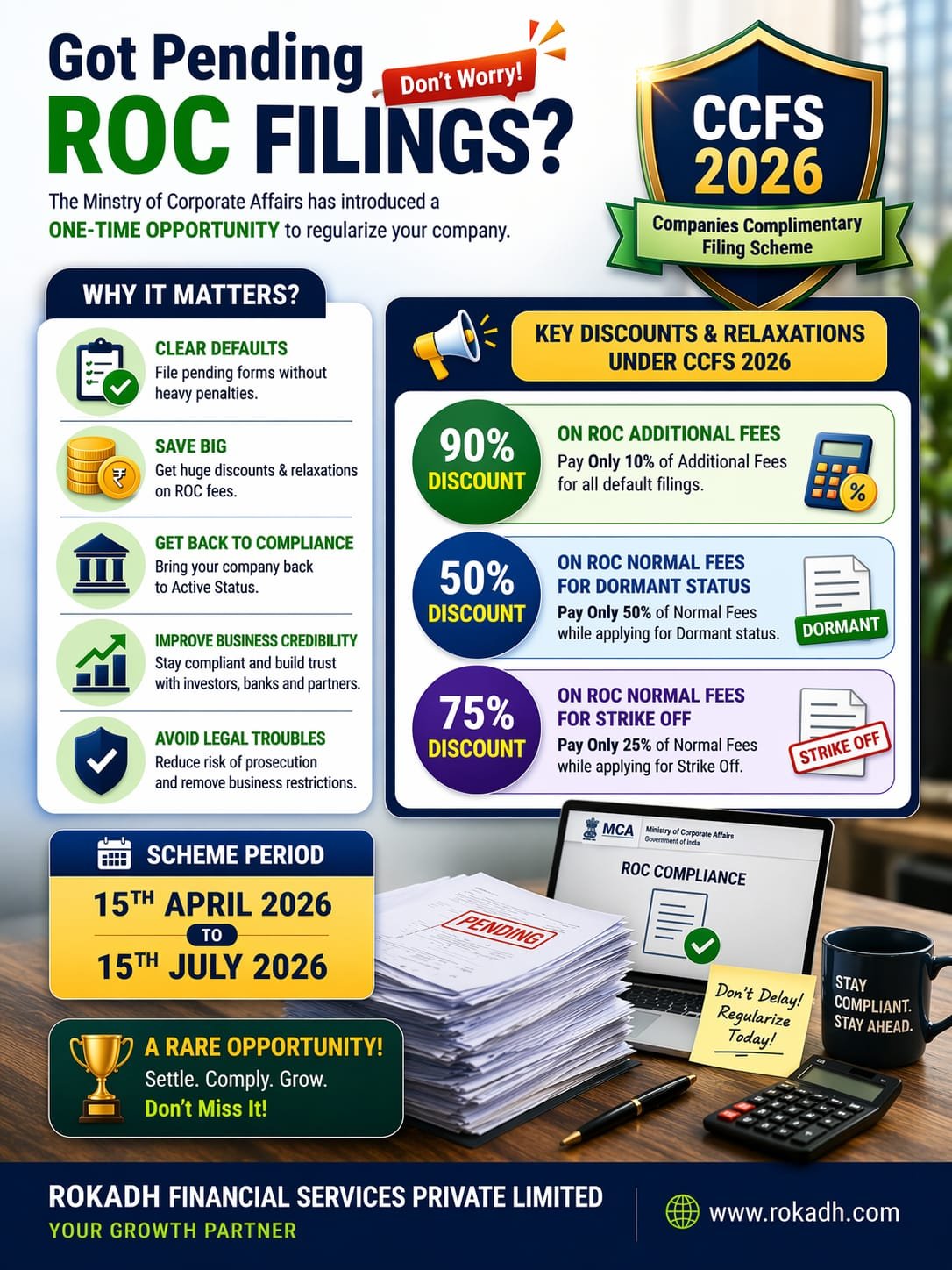

2. Effective Dates of CCFS-2026

The Scheme:

- Commences: 15 April 2026

- Closes: 15 July 2026

This means companies get 90 days only to avail the benefits.

No extension is guaranteed.

After 15 July 2026, strict action under the Act will resume.

3. What Does CCFS-2026 Offer?

Under this scheme, companies have three powerful options:

OPTION 1: File Pending Annual Returns & Financial Statements

Pay Only 10% of Additional Fees

Normally:

- ₹100 per day per form

- No maximum cap

Under CCFS-2026:

- Pay normal filing fee

- Pay only 10% of total additional fee

This is a 90% waiver of additional fees.

OPTION 2: Become a Dormant Company

Pay Only 50% of Normal Fee

Companies can:

- File e-Form MSC-1

- Obtain dormant status under Section 455

- Pay only half of normal filing fee

Dormant status allows:

- Minimal compliance

- No heavy annual filing burden

- Retention of corporate identity

Ideal for temporarily inactive businesses.

OPTION 3: Strike Off the Company

Pay Only 25% of Filing Fee

Companies can:

- File e-Form STK-2

- Apply for removal of name

- Pay only 25% of filing fee

Perfect for:

- Defunct companies

- Shell companies

- Promoter-abandoned entities

4. Relevant E-Forms Covered Under CCFS-2026

The scheme applies to the following:

Under Companies Act, 2013:

- MGT-7

- MGT-7A

- AOC-4

- AOC-4 CFS

- AOC-4 NBFC (Ind AS)

- AOC-4 CFS NBFC (Ind AS)

- AOC-4 XBRL

- ADT-1

- FC-3

- FC-4

Under Companies Act, 1956:

- Form 20B

- Form 21A

- Form 23AC

- Form 23ACA

- Form 23AC-XBRL

- Form 23ACA-XBRL

- Form 66

- Form 23B

Thus, both old and new regime filings are covered.

5. Applicability – Who Can Avail CCFS-2026?

The scheme applies to all companies, except the following:

Not Eligible:

- Companies against which final notice for strike off under Section 248 has already been initiated

- Companies that have already filed application for strike off

- Companies that applied for dormant status before scheme commencement

- Companies dissolved pursuant to amalgamation

- Vanishing companies

If your company does not fall under these categories, you can avail the scheme.

6. Immunity from Penalty – A Crucial Benefit

This is one of the most important parts of CCFS-2026.

For Sections 92 & 137 Defaults:

If filings are made:

- Before issuance of notice by adjudicating officer

- OR

- Within 30 days of issuance of notice

Then:

- Proceedings shall be concluded

- No penalty shall be levied

However:

If adjudication order already passed OR 30 days expired:

- Penalty liability remains

- Scheme only reduces additional filing fees

For Certain Other Forms (e.g., ADT-1 etc.)

Immunity available if:

- Forms filed under scheme

- No prosecution filed

- No adjudication proceedings initiated before filing

7. Practical Financial Impact – Illustration

Let’s assume:

Company defaulted for 2 years in filing AOC-4 & MGT-7.

Additional fee calculation:

₹100 × 365 × 2 years = ₹73,000 per form

For 2 forms = ₹1,46,000 additional fee

Under CCFS-2026:

Only 10% payable = ₹14,600

Savings = ₹1,31,400

For MSMEs, this is massive relief.

8. Strategic Decision Framework – What Should Companies Do?

Not every company should simply file returns.

You must evaluate:

Scenario A: Business Active

→ File pending returns

→ Clean compliance history

→ Avoid director disqualification

→ Restore banking credibility

Scenario B: Temporarily Inactive

→ Opt for Dormant Status

→ Reduce compliance burden

→ Maintain corporate shell for future

Scenario C: Business Closed

→ Apply for Strike Off

→ Avoid future penalties

→ Close entity cleanly

At Rokadh, we recommend strategic evaluation before filing blindly.

9. Risks If You Ignore CCFS-2026

After 15 July 2026:

- ROC may initiate adjudication

- Heavy penalties may be imposed

- Director disqualification risk

- DIN deactivation

- Prosecution proceedings

- Company strike off

This scheme is not just an opportunity — it is a compliance reset window.

10. Step-by-Step Process to Avail Scheme

Step 1: Compliance Audit

Identify pending filings.

Step 2: Financial Reconstruction

Prepare financial statements.

Step 3: Conduct Board Meetings

Approve accounts.

Step 4: Hold AGM (if required)

Step 5: File AOC-4 & MGT-7

Step 6: Pay 10% additional fees

OR

File MSC-1 / STK-2 as applicable.

Professional assistance is strongly recommended.

11. Impact on Directors

Non-filing affects:

- Director DIN status

- Director reputation

- Bank compliance

- Loan approvals

- Tender participation

Regularization improves director profile.

12. Impact on MSMEs & Startups

Startups often ignore compliance during early struggles.

This scheme:

- Prevents long-term financial damage

- Avoids heavy ROC burden

- Encourages formalization

For MSMEs, this is survival support.

13. Corporate Governance Perspective

A clean registry:

- Improves investor confidence

- Enhances regulatory transparency

- Reduces shell company misuse

- Strengthens formal economy

CCFS-2026 aligns with India’s governance reforms.

14. Important Legal References

- Section 92 – Annual Return

- Section 137 – Financial Statements

- Section 403 – Fees & Additional Fees

- Section 455 – Dormant Company

- Section 460 – Condonation of Delay

- Section 248 – Strike Off

15. Key Takeaways

- 90% waiver of additional fees

- 50% fee for dormant status

- 75% concession on strike off

- Limited 90-day window

- Immunity benefits available

- Strict action after closure

16. How Rokadh Financial Services Can Help

At Rokadh Financial Services Private Limited, we assist with:

✔ Complete compliance audit

✔ Preparation of financial statements

✔ Back-dated compliance structuring

✔ AGM regularization

✔ E-filing under CCFS-2026

✔ Dormant application strategy

✔ Strike off advisory

✔ Director risk advisory

Our approach is strategic — not mechanical filing.

We help you decide the best compliance path.

17. Final Advisory Note

CCFS-2026 is not a routine circular.

It is a compliance reset mechanism.

For many companies, this may be the last opportunity to regularize without facing heavy penalties.

If your company has pending filings, the question is not:

“Should we file?”

The question is:

“Can we afford not to?”

Conclusion

The Companies Compliance Facilitation Scheme, 2026 represents a balanced regulatory intervention:

- Relief for genuine defaulters

- Discipline for habitual non-compliance

- Transparency in registry

- Ease of doing business

Companies must act between:

15 April 2026 – 15 July 2026

After that, enforcement returns to full force.